This is part of a 4-part series exploring where AI is impacting major industries that power NYC.

Much like the internet, the PC, and the semiconductor, AI is too consequential to stay confined to one sector. Every industry will look measurably different in ten years, and AI will deserve much of the credit. The race now isn’t just to build it. It’s to use it.

Few industries will matter more in that transition than financial services. The industry is massive, operationally complex, and filled with high-value workflows that remain surprisingly manual. Banks spend roughly $600B a year on technology, yet 43% of banking systems still rely on COBOL..That combination makes it one of the most obvious places for AI to land, and one of the hardest places to deploy successfully.

As a NYC-based venture firm deep in enterprise technology since 2013, we've had a front-row seat to how applied AI is beginning to reshape the financial institutions headquartered here, and what it actually takes to make that happen inside complex, high-stakes organizations.

Here’s what we’re seeing.

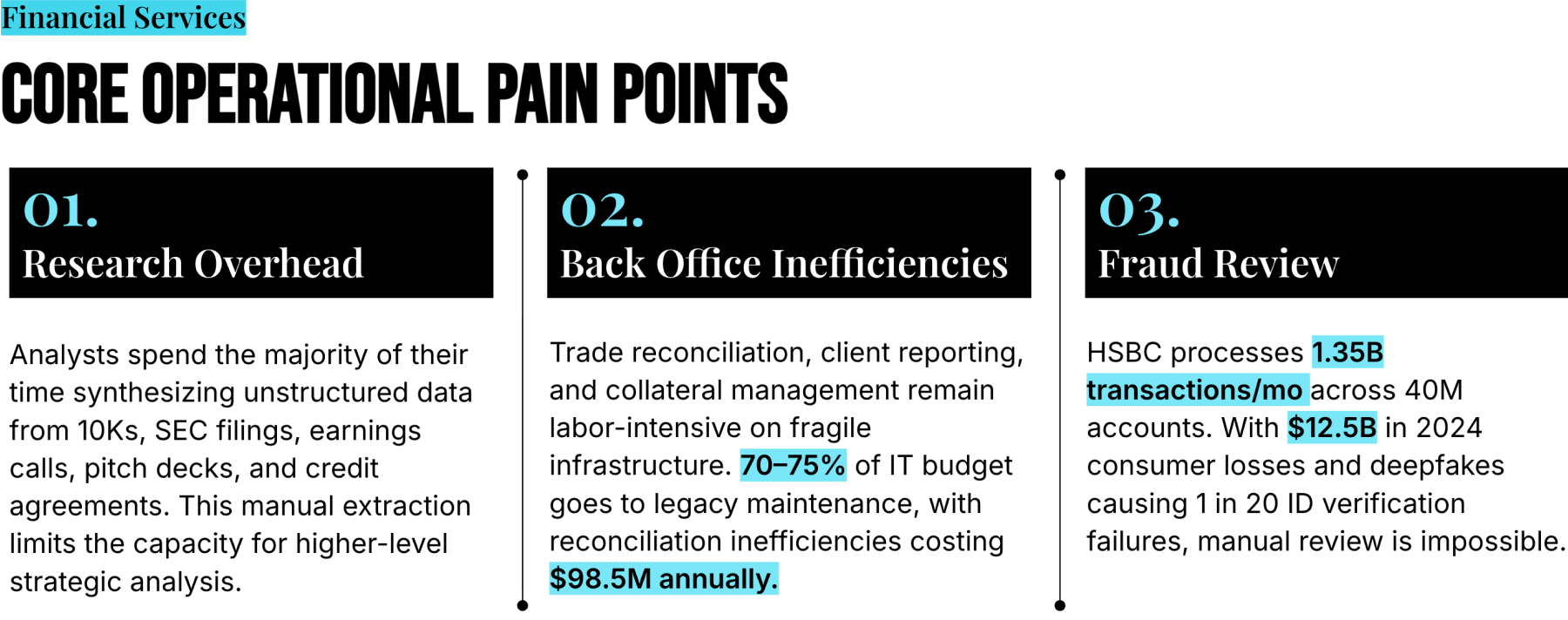

The pain points

A few areas where AI can have an immediate impact stand out:

- Research overhead: Spend a day shadowing an investment banking analyst. Much of their time will be spent synthesizing 10Ks, SEC filings, earnings calls, pitch decks, and credit agreements.

- Back office inefficiencies: Much of financial services still runs on operational processes that are manual and built on fragile legacy infrastructure. Trade reconciliation, client reporting, collateral management, and other core workflows are labor intensive. Banks spend ~70-75% of their IT budget on maintaining legacy systems, and reconciliation inefficiencies alone cost firms $98.5M annually.

- Fraud review: Scale makes manual review impossible. HSBC, for example, processes 1.35 billion transactions monthly across 40 million customer accounts. Total consumer fraud losses exceeded $12.5B in 2024, and only one-third of financial organizations detect fraud at onboarding, with most catching it later in the transaction flow. The problem is also evolving as AI continues to create more convincing deepfakes, which are now responsible for 1 in 20 identity verification failures.

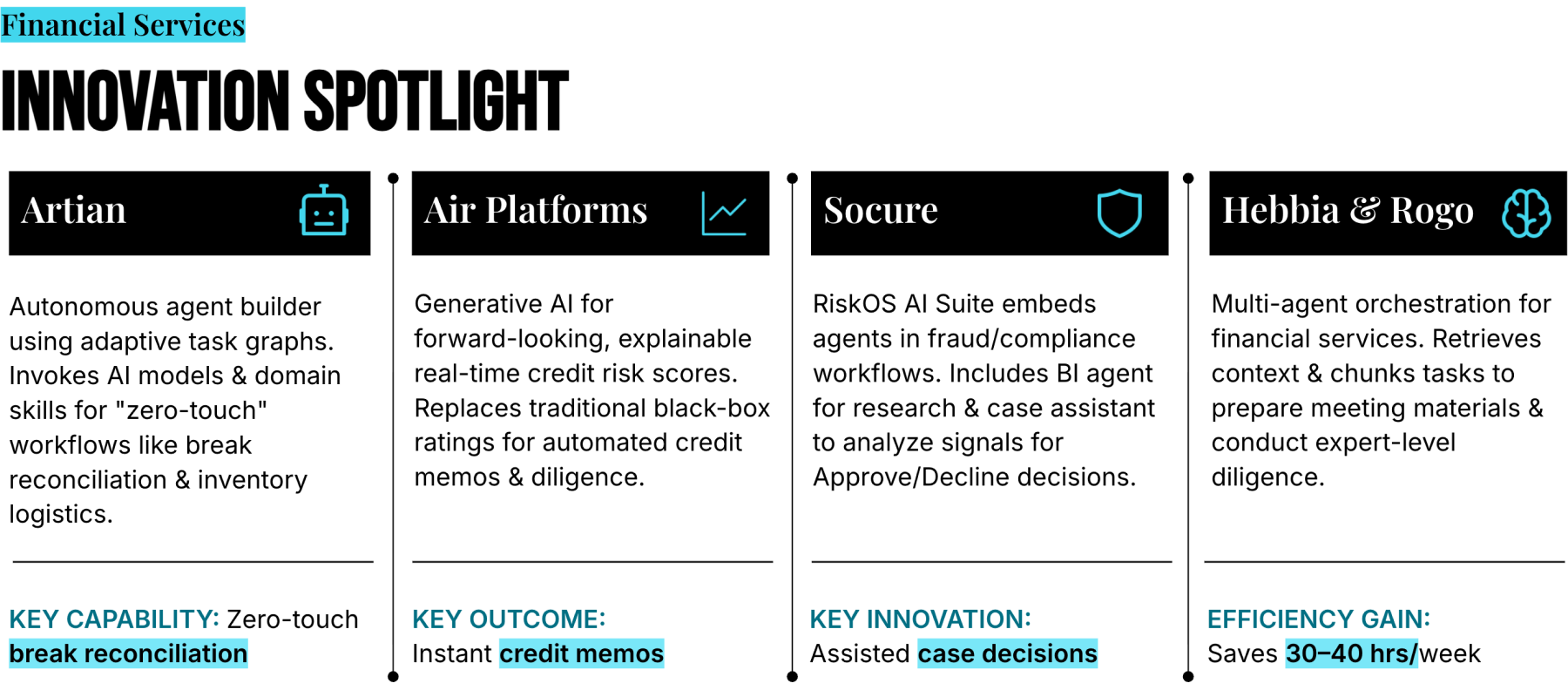

Where AI can help

Several companies are already applying AI to these workflows:

- Our portfolio company Artian has built an autonomous agent builder, which is essentially an IDE for reliable, structured agents. The agents complete work using adaptive task graphs, which invokes AI models as well as domain-specific skills. While it's still early days, Artian agents have already seen use cases ranging from break reconciliation in trading operations to inventory logistics in derivatives trading.

- Our portfolio company AIR Platforms uses generative AI to ingest massive amounts of data (both structured and unstructured) to deliver forward-looking, explainable, real-time credit risk scores, replacing traditional credit ratings that come with lag, limited coverage, and black-box methodologies. The company also generates automated credit memos, diligence packages, and scenario analyses (work that might take a team hours).

- Our portfolio company Socure recently debuted their RiskOS AI Suite, which embeds agents into every fraud, compliance, and risk decisioning workflow (think consumer/business onboarding, user verification, comprehensive bank account verification, etc). This includes a business intelligence agent (automates business research across websites, social profiles, and registries to surface legitimacy and risk in seconds) and a case assistant agent (analyzes all scores, signals, and historical outcomes in a case to suggest most likely outcome—Approve, Escalate, Decline, or Fraud).

- Hebbia and Rogo have built application platforms for financial services firms. Hebbia's platform has helped bankers save 30-40 hours per week preparing meeting materials, and has helped PE firms save 20-30 hours per deal on due diligence and expert level research. It’s made possible both by the raw intelligence of the LLM and the design of the system surrounding it, from retrieval of vast amounts of context to chunking tasks into manageable steps and routing prompts to the best possible model.

Things to keep in mind

- Relationships Are Still Paramount: As much as AI can automate work, it cannot automate the trust that wins the business. The great banks win on relationships and brand value compounded over decades, and that human-to-human dynamic only becomes more important as work moves faster and gets cheaper. Also, accountability still sits with people: AI can accelerate the analysis but high-stake decisions in financial services must be explainable and defensible to both regulators and clients.

- Legacy Infra Slows AI Deployment: AI adoption will naturally be fast with startups running on the latest infrastructure, but what about banks still running on COBOL? There is a nontrivial amount of change management and implementation work for AI to actually make its way into production. Everyone’s stack looks different.

- Regulation Shapes Adoption: Financial services is one of the most regulated industries in the US, where “move fast and break things” doesn’t quite work. The long sales cycles and meaty customer contracts exist for a reason. Making sure guardrails and risk infrastructure are in place to minimize the downside of stochastic AI behavior is incredibly important.

Financial services is one of those industries where AI is hardest to deploy and most valuable once it lands. What stands in the way of seamless AI adoption is trust, legacy infrastructure, and a regulatory environment that doesn't tolerate "move fast and break things." The companies that figure out how to navigate that complexity while still delivering real workflow-level impact will be the ones who build truly durable businesses. We're excited to keep watching this space closely.